The Long-Game Strategy: Masterful Homeownership and Financial Planning

Many homeowners view their property as a monthly expense rather than a dynamic engine for long-term wealth. True financial sovereignty requires moving beyond the “survival mode” of paying bills and entering a proactive state of strategic management. By adopting a multi-decade perspective, you can transform a primary residence from a simple shelter into a foundational asset that supports your broader life goals.

A long-term mindset in personal finance involves prioritizing future stability over immediate gratification. It requires a commitment to proactive maintenance, strategic debt restructuring, and consistent investment planning to ensure that your home remains a source of equity rather than a drain on your liquid capital.

The Foundation of Financial Foresight

The journey toward sustainable homeownership begins with a fundamental shift in how you view debt and equity. Most people react to financial pressure as it arises, but high-authority planners anticipate shifts in the economy. For instance, understanding the broader landscape of consumer behavior can help you time your large purchases or renovations. You can find detailed analysis on current spending trends in the Federal Reserve Survey of Consumer Finances.

Proactive decision-making also involves managing the liabilities that sit alongside your mortgage. If you find yourself carrying high-interest debt that competes with your ability to maintain your property, you might consider financial tools designed to lower your interest burden. Using balance transfer cards strategically can help homeowners reduce high-interest debt, freeing up more money for long-term financial goals like home maintenance, emergency savings, and mortgage payments. To see how different options stack up against one another, you can compare balance transfer cards on BestMoney.com to find a promotional window that aligns with your specific repayment timeline.

The Home Equity Preservation Model

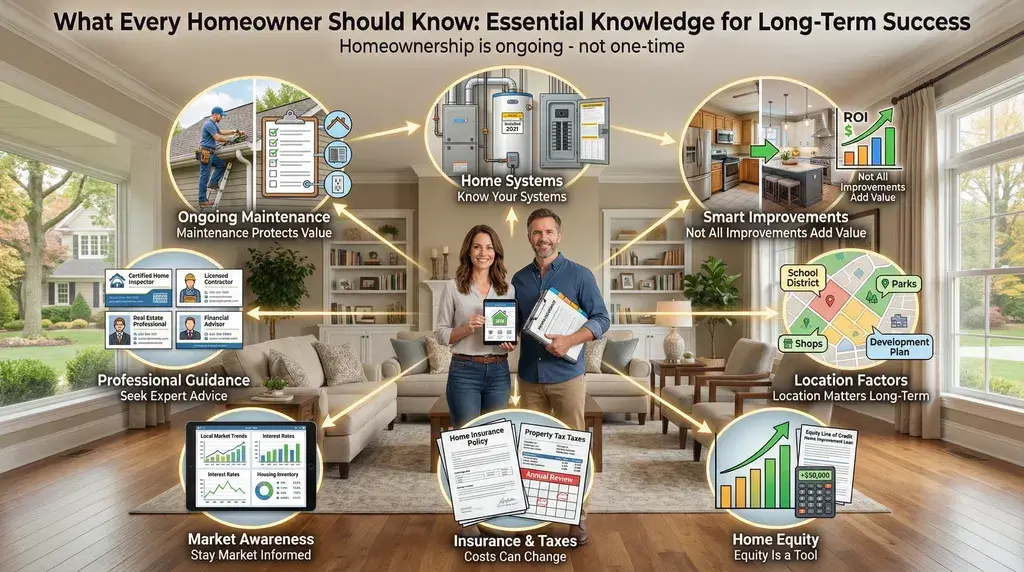

To navigate the complexities of property ownership, plan ahead for upkeep. A common rule of thumb is to set aside roughly 1% of your home’s value each year for maintenance and repairs. Skipping this step can lead to deferred maintenance, where small issues compound and your home loses value faster than the market can lift it.

Managing your cash flow is the most critical component of this protocol. When you reduce the interest you pay on credit cards or personal loans, you create a surplus that can be funneled into an emergency repair fund. It is vital to evaluate the specific terms of any debt consolidation tool, such as the length of the introductory period and the associated fees, which usually range from 3–5%.

Strategic Cost Management and Growth

As your equity grows, your opportunities for expansion often follow. Many successful individuals transition from owning a single home to diversifying their portfolio through additional real estate holdings. This transition requires a high level of professional guidance to avoid common pitfalls in property management and local market fluctuations. If you are looking to scale your assets, it is often wise to explore investment properties with the help of seasoned experts who understand the nuances of the local landscape.

Data from recent years shows that consistent, small improvements to financial health lead to much larger gains than trying to “time” the market perfectly. The following table illustrates the potential impact of different financial focuses over a five-year period.

Financial Planning Impact Comparison

Focus Area | Short-Term Action | Long-Term Benefit |

Debt Management | Reducing interest rates | Increased monthly cash flow |

Home Maintenance | Seasonal inspections | Prevention of major repair costs |

Investment | Diversified assets | Protection against market volatility |

Savings | Automated transfers | Robust emergency safety net |

The key is to avoid becoming overwhelmed by the scale of your goals. Instead, focus on the immediate, actionable steps that lead to long-term stability. Government resources often provide data that can help you understand how your housing costs compare to national averages, which is essential for benchmarking your progress. You can review the latest Consumer Expenditure Survey to see how typical households allocate their funds toward housing and related expenses.

Essential Steps for Proactive Homeowners

● Conduct a full audit of all high-interest liabilities every six months.

● Allocate a minimum of one percent of your home’s value for annual upkeep.

● Review your mortgage terms against current market rates annually.

● Automate your savings to ensure the house fund grows without manual effort.

How to Execute a Long-Term Financial Plan

- Analyze your current debt-to-income ratio to identify areas for improvement.

- Establish a dedicated “Home Health” savings account.

- Consult with a professional to integrate your home equity into your retirement plan.

- Research local property trends by looking at FHFA House Price Index reports to understand your asset’s performance.

- Develop a five-year renovation schedule based on the age of your home’s major systems.

True wealth is built through the accumulation of smart choices over time. For those looking for deeper insights into how demographics affect housing and finance, the Census Bureau housing data offers a look at current vacancy rates and homeownership trends across the country. By staying informed and acting decisively, you can ensure your home remains your greatest financial ally. Utilizing the expertise of a Franklin Investment Realty professional can further refine your approach to real estate as a vehicle for wealth.

Common Financial Questions

How can I lower my monthly housing costs without refinancing?

You can lower costs by appealing your property tax assessment, increasing your insurance deductible, or using high-yield savings to offset interest expenses.

What is the best way to handle unexpected home repairs?

Maintaining a dedicated emergency fund that covers at least six months of expenses is the most effective way to manage surprise costs without taking on new debt.

When should I consider an investment property?

An investment property is worth considering when your primary mortgage is manageable, you have a stable cash reserve, and you have identified a market with strong rental demand.

Does paying off a mortgage early always make financial sense?

Not necessarily. If your mortgage interest rate is lower than the return you could get from a diversified investment portfolio, it may be better to invest the surplus funds.

How do I balance retirement savings with home improvements?

Prioritize improvements that prevent structural damage first, as these protect the asset’s value. Use a percentage-based budget to ensure retirement contributions remain consistent.

Conclusion

Embracing a long-term mindset is the most effective way to secure your financial future. By treating homeownership as a series of proactive choices rather than a static obligation, you position yourself to thrive in any economic climate. Focus on the fundamentals of debt management, consistent maintenance, and professional collaboration to turn your vision of financial independence into a tangible reality.

– Shirley Martin